Alphabet’s Big Bet

Why A.I. is the existential threat

Alphabet’s scale and size can be a complicated story for people to understand. The aim of this essay is to help people understand it.

Do Alphabet Shareholders Need to Worry?

For many years, Alphabet looked like the perfect modern technology company: dominant, profitable, cash-generative, asset-light, and able to return huge amounts of money to shareholders through buybacks.

Google Search threw off cash. YouTube grew. Cloud improved. The company had so much financial strength that it could invest heavily, pay employees richly, absorb regulatory fines, fund moonshots, and still buy back tens of billions of dollars of its own shares.

Those buybacks mattered. They reduced the share count. They supported earnings per share. They gave investors confidence that Alphabet’s cash machine was not just producing growth, but returning value. For shareholders, the story was simple: Alphabet owned one of the great toll roads of the digital economy, and the toll road was producing more cash than the company could sensibly spend.

That is why the latest capital raise matters.

Alphabet has spent roughly $348 billion buying back its own shares since the start of its repurchase programme in 2015. In recent years alone, it spent $62.2 billion in 2023, $62.0 billion in 2024, and $45.4 billion in 2025. Even at the end of 2025, it still had around $69.5 billion authorised for future buybacks.

Now the company is reportedly raising up to $84.75 billion in new equity capital to help fund its AI infrastructure build-out.

That is the symbolic shift.

Alphabet is moving from a world of surplus cash return to a world of external capital funding. The company that spent years shrinking its share count is now issuing capital to fund the next phase of the technology race.

This does not mean Alphabet is weak. It does not mean the company is broken. But it does mean the shareholder contract has changed.

The question is no longer simply:

Can Google keep generating cash?

The question is now:

Can Alphabet earn a high enough return on the vast amount of capital it is about to deploy?

That is a very different question.

The Scale of the New Capital Cycle

The proposed Alphabet raise is enormous, but it is no longer unusual in the new AI economy.

OpenAI has announced $122 billion in committed capital. Anthropic has announced a $65 billion funding round. SpaceX is reportedly targeting a $75 billion IPO raise. Alphabet’s proposed $84.75 billion raise sits in the same broad capital-market conversation.

That is remarkable.

Alphabet is not a start-up trying to prove product-market fit. It is one of the most profitable companies in the world. It has Search, YouTube, Android, Google Cloud, Gmail, Maps, DeepMind, Gemini, advertising infrastructure, custom chips, global data centres and enormous distribution.

And yet even Alphabet is now raising external capital.

That tells us something important about AI.

AI is not just another software wave. It is an infrastructure wave.

It needs data centres, chips, power, cooling, land, fibre, energy contracts, model training, inference capacity and constant reinvestment. It is not simply code. It is industrial infrastructure wearing a software mask.

That is why markets are nervous.

Investors like growth. They are less comfortable when growth requires huge upfront spending before the returns are clear. They become especially nervous when every major player believes it has no choice but to spend.

That is the dangerous sentence in any capital cycle:

We cannot afford to fall behind.

Once every major company believes it cannot afford to fall behind, capital discipline becomes harder. Spending becomes defensive as well as strategic. The investment case moves from opportunity to arms race.

From Buyback Compounder to Infrastructure Builder

For years, Alphabet’s shareholder appeal was beautifully simple.

It was a growth company with monopoly-like economics in parts of its business. It was a quality compounder. It could invest in the future and still return cash. Conservative growth investors, index funds, long-term institutions and quality-focused shareholders could all own it with a degree of comfort.

Buybacks reinforced that comfort.

They said: we are so cash-generative that we can reduce the share count while still funding growth.

A large capital raise says something different.

It says: the next phase of growth may require more capital than we are willing to fund entirely from existing cash flow.

That does not automatically make it bad. But it changes the nature of the investment.

The old Alphabet was closer to a cash machine with growth options.

The new Alphabet may become an infrastructure-heavy AI platform with far greater capital intensity.

That distinction matters deeply to existing shareholders.

Some shareholders bought Alphabet for quality growth. Some bought it for buybacks. Some bought it for the strength of Search. Some bought it because it looked financially self-sufficient. Some bought it because it was one of the safest ways to own the digital economy.

Those shareholders now face a new question:

Are they still invested in the same kind of company?

The Telco Analogy

The obvious historical analogy is the telecoms boom of the late 1990s and early 2000s.

Back then, the internet was real. Mobile was real. Data traffic was going to grow. The world was going digital. None of that was wrong.

But many telecom companies drew the wrong financial conclusion from the right technological insight.

They believed that because the internet would become huge, every network build-out would be valuable. They raised debt and equity. They bought spectrum. They laid fibre. They built capacity for a future that was indeed coming, but not always at the speed, pricing or profitability they expected.

The result was one of the great capital-cycle lessons of modern markets.

The infrastructure was useful. The internet did grow. The world did become digital. But many of the companies that funded the infrastructure did not receive the reward. Some went bankrupt. Some were taken over. Some survived but never regained their former market glory. The users and later platform companies captured much of the value, while many network builders carried the debt.

That is the uncomfortable question for Alphabet shareholders:

Is Alphabet building the next great profit engine — or is it helping fund the infrastructure layer from which others will also benefit?

The answer is not obvious.

Alphabet is not a weak telecom operator from 2000. It is immensely profitable. It has stronger margins, stronger cash generation, better technology assets, global distribution and more strategic control than many of the telecom companies that got into trouble.

But the telco analogy still matters because it reveals the shareholder dilemma.

Many telecoms were considered blue-chip companies. They were owned by conservative shareholders. They were seen as safe, essential, cash-generative businesses. They had infrastructure, customers, national importance and recurring revenues. They looked solid.

Then the investment case changed.

They moved from being reliable cash-flow businesses to capital-hungry growth stories. Conservative shareholders found themselves funding a speculative infrastructure race. The companies were still important. The technology was still real. The future still arrived.

But the economics changed.

That is the risk for Alphabet.

The company may remain essential. AI may change the world. Demand may grow enormously. But shareholders still need to ask: who captures the value, and at what cost?

What This Means for Existing Shareholders

For existing Alphabet shareholders, the key issue is not whether AI is real. It is.

The issue is whether Alphabet can translate AI infrastructure spending into superior returns per share.

That phrase — per share — is crucial.

A company can grow larger while shareholders do not get richer. Revenue can rise while margins fall. Infrastructure can expand while free cash flow shrinks. AI usage can explode while monetisation disappoints. The company can become more important to the world while becoming less attractive as a stock.

That is what happened to many infrastructure players in previous technology cycles.

Existing shareholders therefore need to watch five things.

First, dilution. Alphabet has spent years using buybacks to reduce the share count. A large equity raise reverses some of that logic. If the company issues shares to fund AI, existing shareholders own a smaller percentage of the future unless the new capital generates returns high enough to compensate.

Second, free cash flow. The market loved Alphabet because it produced huge cash flow. AI infrastructure absorbs cash. If capital expenditure keeps rising faster than operating cash flow, the company becomes less financially flexible.

Third, depreciation. AI infrastructure is not like pure software. Chips, servers and data centres depreciate. Some AI hardware may have shorter useful lives because the technology is improving so quickly. Today’s leading chip can become tomorrow’s older asset.

Fourth, monetisation. AI demand is not the same as AI profit. People may use AI heavily, but will they pay enough? Will advertisers pay more? Will enterprises sign durable contracts? Will AI search protect or weaken Google’s advertising model? Will Gemini and Cloud capture value, or will customers treat models as interchangeable?

Fifth, capital discipline. The biggest danger in any arms race is that the logic of competition overwhelms the logic of returns. If Microsoft, Amazon, Meta, OpenAI, Anthropic, SpaceX and others are all raising or spending vast sums, Alphabet may feel forced to keep spending even when the returns become less certain.

That is the real shareholder worry.

Not that Alphabet cannot afford to spend.

But that it may feel unable to stop.

The Bull Case

The positive case is still powerful.

Alphabet may be doing exactly what it must do.

If AI changes search, advertising, cloud computing, software development, video, enterprise automation, personal assistants and robotics, then Alphabet cannot simply defend the old model. It has to build the new one.

In this version of the story, the capital raise is not a sign of weakness. It is a bridge into the next era.

Alphabet has advantages most companies do not have: data, talent, infrastructure, custom chips, distribution, existing customers, global products and deep AI research. If it can use AI to protect Search, improve advertising, grow Cloud, automate enterprise work, enhance YouTube, strengthen Android and create new products, then today’s spending may become the foundation for another decade of dominance.

In that case, shareholders may look back and say the company did the right thing. It used its balance sheet and market credibility to secure the infrastructure needed for the next platform shift.

The telecom analogy would then be incomplete. Alphabet would not be the overbuilt network operator. It would be more like the company that owns both the network and the services that run on top of it.

That is the optimistic outcome.

The Bear Case

The negative case is also clear.

Alphabet could spend too much, too quickly, in a market where every competitor is also spending too much, too quickly.

AI capacity could become overbuilt. Pricing could fall. Models could commoditise. Customers could use more AI but resist paying enough for it. Regulators could restrict data use, advertising practices or market power. Search behaviour could shift in ways that damage the advertising model before new AI revenues fully replace it.

In this version, Alphabet remains a great company but becomes a less attractive investment.

Margins compress. Free cash flow weakens. Buybacks slow. Depreciation rises. The share count stops shrinking. The market applies a lower valuation multiple because the company now looks more capital-intensive and less predictable.

This would not necessarily mean collapse.

Alphabet is much stronger than many telecom companies were during the 2000 crash. It has more profit, more control, more products and a better balance sheet. But shareholders do not need a collapse to suffer disappointment. A great company can still deliver poor returns if expectations are too high and capital returns are too low.

That may be the more realistic risk: not disaster, but derating.

The Middle Case

The most likely outcome may sit between triumph and disaster.

Alphabet probably remains one of the most important companies in the world. AI probably becomes deeply embedded across its products. The company probably keeps generating large profits. But the easy era of buyback-led compounding may fade.

The business may become more cyclical, more capital intensive and more difficult to value.

Shareholders may need to accept lower buybacks, higher capital expenditure, more volatility and a longer wait before AI returns become visible. Some conservative investors may decide that this is no longer the same type of holding. Others may see the capital raise as the price of staying relevant.

This is where the telco comparison becomes most useful.

The mistake is not investing in infrastructure. Infrastructure creates the future.

The mistake is assuming that because the future needs infrastructure, every infrastructure investor will earn attractive returns.

That is the distinction shareholders must keep in mind.

So What Will Happen to Alphabet?

No one can know with certainty.

But the likely answer is that Alphabet will survive, adapt and remain powerful. This is not a simple repeat of the telecom bust. The company is too profitable, too diversified and too strategically embedded to be compared directly with the weaker, heavily indebted telecom companies of the late 1990s.

But Alphabet’s stock may begin to behave differently.

It may be valued less like a pure software platform and more like a hybrid of technology, infrastructure and utility. Investors may focus less on revenue growth and more on return on invested capital. They may demand evidence that AI spending is producing durable margins, not just usage. They may become less forgiving of vague promises and more focused on cash conversion.

For existing shareholders, this means the question changes.

It is no longer enough to believe in Google.

It is no longer enough to believe in AI.

They must believe that Alphabet can turn AI spending into attractive per-share economics.

That is the test.

The Final Judgement

So, do Alphabet shareholders need to worry?

Yes — but not because Alphabet is suddenly weak.

They need to worry because the company has entered a new capital cycle. The old model was simple: generate cash, invest enough to grow, and return the surplus. The new model is more demanding: raise capital, spend aggressively, build infrastructure ahead of demand, and hope that AI revenue grows fast enough to justify the scale.

This is not automatically bad. Some of the greatest fortunes are made when companies invest heavily before the market fully understands the size of the opportunity.

But some of the greatest losses are also made that way.

The lesson of the 1990s telecom boom is not that infrastructure investment is foolish. Without that investment, the modern internet and mobile world would not exist. The lesson is subtler: the infrastructure can be world-changing while the economics disappoint many of the investors who funded it.

Alphabet may avoid that fate because it has distribution, profits, data, engineering, products and customer relationships that the old telecom builders often lacked.

But shareholders should watch carefully.

The question is no longer whether Alphabet can generate cash. It can.

The question is whether it can turn this new wave of AI capital spending into returns that exceed the cost of dilution, debt, depreciation and competitive pressure.

That is the real test.

Alphabet is not in trouble yet. But it is no longer merely a buyback-powered compounder. It is becoming an infrastructure-heavy AI company. That may be the right move. It may even be necessary.

But it is a different game.

And when the game changes, shareholders should always pay attention.

How can Shareholder’s assess The company’s decision making?

What has been Google/Alphabet’s track record in Investments, Acquisitions and Internet Projects/Moonshots?

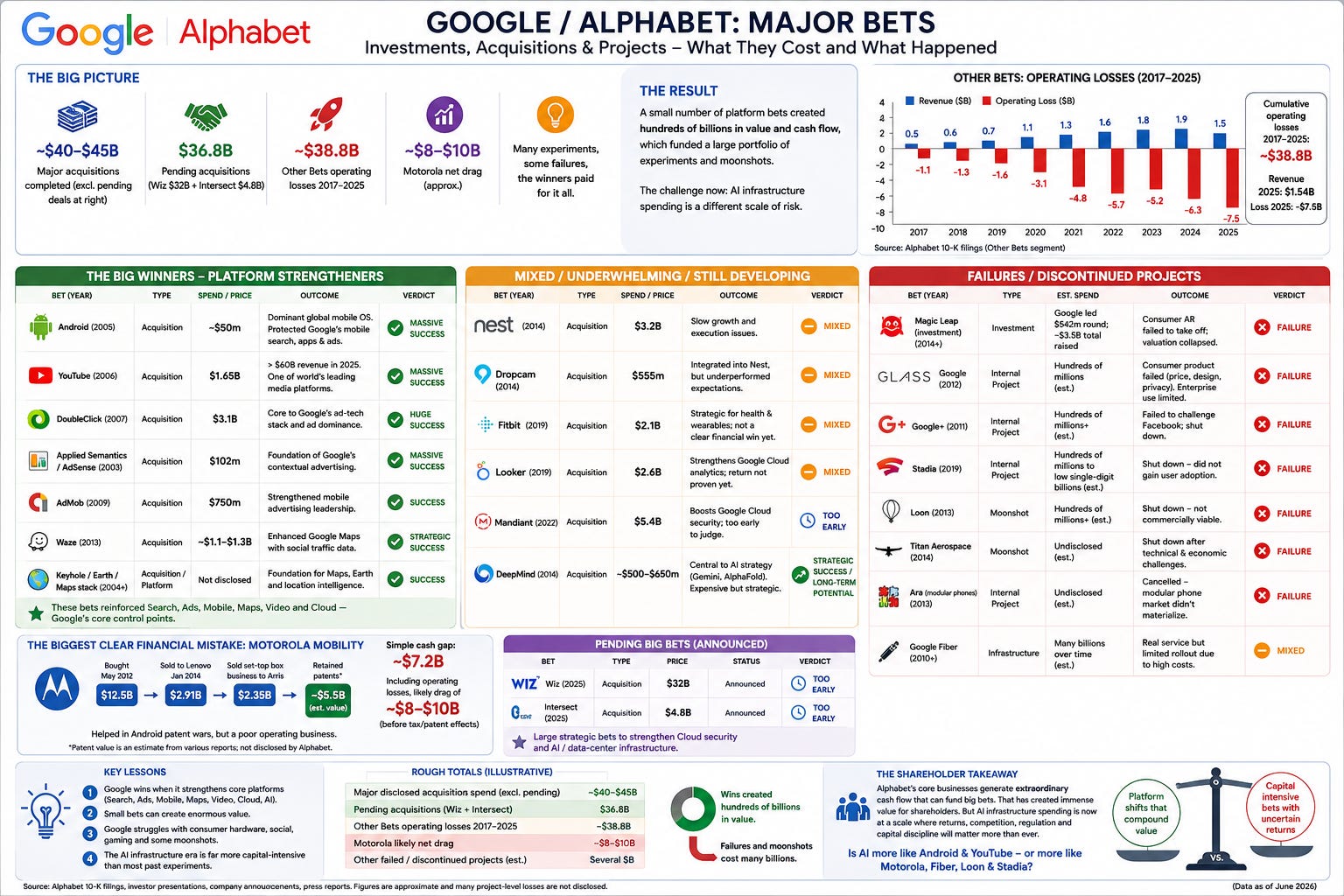

Google/Alphabet’s Big Bets: What Worked, What Failed, and What It Means for Shareholders

The clearest way to understand Google and Alphabet’s investment history is this: the company has had an extraordinary record when it bought or built things that strengthened its core control points — search, advertising, maps, mobile, video, cloud and AI. It has been much weaker when it tried to become a consumer hardware company, a social network, a gaming platform, a telecoms provider, or a speculative moonshot factory.

That is the important distinction.

The big lesson for shareholders is not simply that “Google wastes money.” That is too crude. The subtler truth is that Alphabet has been able to absorb many failures because Search and Ads have been so profitable. A normal company could not afford this level of experimentation. Alphabet could. The concern today is that the new AI infrastructure cycle is much larger than most of its past experiments. AI is not a small acquisition or an isolated product failure. It is a capital cycle involving chips, data centres, power, cooling, cloud capacity and long-term infrastructure commitments.

So the question is not whether Google has made mistakes before. It has. The question is whether AI will be more like Android and YouTube — a platform shift Alphabet had to own — or more like Motorola, Fiber, Glass, Loon and Stadia — a technologically real but financially disappointing capital-heavy bet.

The Platform Winners

Google’s greatest successes came when it acquired or built assets that strengthened its position at the centre of the digital world.

Android is probably one of the greatest acquisitions in technology history. Google reportedly bought Android for around $50 million. At the time, it was a small acquisition. In hindsight, it protected Google’s future. Android became the dominant global mobile operating system and ensured that Google Search, Google apps, advertising and services remained deeply embedded in the mobile era. The direct value of Android is not separately reported, but strategically it is likely worth hundreds of billions of dollars to Alphabet.

YouTube is another extraordinary example. Google bought YouTube in 2006 for $1.65 billion. At the time, many observers thought the price was high. YouTube was growing fast but was expensive to run and carried copyright, bandwidth and monetisation risks. Yet over time it became one of the world’s most important media platforms. By 2025, Alphabet said YouTube revenue across advertising and subscriptions exceeded $60 billion. Early losses were real, but the long-term return has been exceptional. YouTube did not just become a business; it became a control point for global video attention.

DoubleClick was also a major success. Google acquired it for $3.1 billion, and it became central to the company’s advertising technology stack. DoubleClick helped Google deepen its control of digital advertising infrastructure, linking publishers, advertisers, data and ad serving. It created enormous strategic value, although it also became part of Google’s later regulatory and antitrust problems. In financial and strategic terms, it was a huge win. In political and regulatory terms, it added long-term risk.

Applied Semantics, which helped form the basis of AdSense, was another small acquisition with enormous consequences. Google reportedly paid around $102 million for the company. That acquisition helped strengthen Google’s contextual advertising machine, allowing it to match ads to web pages and expand beyond search advertising. Relative to the purchase price, the return was extraordinary.

AdMob followed a similar pattern. Google bought AdMob for $750 million, strengthening its position in mobile advertising as apps became central to internet usage. The standalone profit is difficult to isolate, but strategically it helped Google dominate advertising in the mobile era.

Waze was another smart strategic acquisition. Google reportedly paid around $1.1 billion to $1.3 billion for Waze. On its own, Waze may not have become a huge direct profit engine, but it strengthened Google Maps with social traffic data and prevented a competitor from owning a critical navigation layer. The value was not simply the app; it was the protection and enhancement of Google’s location intelligence.

Keyhole, which became part of Google Earth and the broader Maps stack, was also strategically important. The purchase price was not fully disclosed, but the impact was significant. Google Earth, Maps and location intelligence became foundational to local search, Android, advertising, navigation and consumer behaviour. Again, the pattern is clear: Google wins when it strengthens a core platform.

These successes share one characteristic. They were not usually enormous at the time of acquisition. Android, YouTube, Applied Semantics, AdMob and Waze were small compared with the value they later created. They worked because they reinforced Google’s control points: search, advertising, mobile, maps, video and data.

The Mixed and Underwhelming Bets

Alphabet’s record becomes more mixed when it moves into hardware, consumer devices, enterprise acquisitions and businesses outside its deepest strengths.

Motorola Mobility is the clearest example of a large, visible financial mistake. Google bought Motorola Mobility for $12.5 billion. It later sold the handset business to Lenovo for $2.91 billion and the set-top box business to Arris for $2.35 billion. On a simple cash basis, this leaves a gap of roughly $7.2 billion. Google did retain patents, and some estimates valued those patents at around $5.5 billion, so the true economic loss is not simply purchase price minus sale proceeds. However, Motorola also generated operating losses while Google owned it, so a rough shareholder-impact estimate of $8 billion to $10 billion of drag is reasonable, before adjusting for patents and tax effects.

The lesson from Motorola is nuanced. It was not totally irrational. It helped Google protect Android during the smartphone patent wars and gave the company leverage in the mobile ecosystem. But as an operating business, it was a poor use of capital. It showed that Google was much better at software ecosystems than at running a traditional handset manufacturer.

Nest is another mixed case. Google bought Nest for $3.2 billion, hoping to build a major smart-home platform. Nest had brand appeal, design credibility and a clear role in the connected-home story. But growth was slower and more troubled than expected. Nest became part of Google’s hardware and smart-home ecosystem, but it never became a YouTube- or Android-style success. It was not a total failure, but it was underwhelming relative to expectations.

Dropcam, acquired for $555 million under Nest, followed a similar path. It became part of the Nest camera product line, but the acquisition was accompanied by founder tensions and execution issues. It likely underperformed the original vision.

Fitbit, acquired for $2.1 billion, helped Google enter wearables, health tracking and the smartwatch market. It supported Pixel Watch and Wear OS, but it is not yet clear that Fitbit has become a major financial success. Strategically, it gave Google a place in health and wearables. Financially, the jury is still out.

Looker, bought for $2.6 billion, strengthened Google Cloud’s data analytics offering. This was a more natural fit for Alphabet because it supported Cloud, enterprise data and analytics. However, no standalone profit is disclosed, so it is difficult to judge whether Looker has become a home run. It is probably useful, but not yet proven as a spectacular acquisition.

Mandiant, acquired for $5.4 billion, strengthened Google Cloud’s cybersecurity capabilities. This also fits the pattern of supporting a core strategic priority: enterprise cloud. But it is still too early to judge the full return.

DeepMind is one of the most important and complicated cases. Google reportedly acquired DeepMind for around £400 million, or roughly $500 million to $650 million. DeepMind produced AlphaGo, AlphaFold and became central to Alphabet’s AI capabilities, including Gemini-related work. It also generated years of heavy losses. From a narrow financial standpoint, DeepMind was expensive. From a strategic standpoint, it may become one of Alphabet’s most important acquisitions. If AI becomes the next dominant platform shift, DeepMind may look like a visionary purchase.

The Failures and Discontinued Projects

Google’s failures reveal a different pattern. The company often understands the technology before it understands the human adoption system.

Magic Leap is a good example. Google led a $542 million funding round, while Magic Leap raised around $3.5 billion overall. The promise was consumer augmented reality. The reality was much harder. The product did not create a mass consumer market, the valuation collapsed from earlier levels, and the company pivoted towards enterprise. Google’s exact loss is not publicly disclosed, but it was likely a paper loss in the hundreds of millions. The broader lesson is that impressive technology does not automatically create a market.

Google Glass failed for similar reasons. The technology was interesting, but the consumer proposition was not right. The product was expensive, socially awkward, poorly understood and surrounded by privacy concerns. It later survived for a time in enterprise contexts, but as a consumer product it failed. No audited project-level loss is available, but the cost was likely in the hundreds of millions over time.

Google+ was a major attempt to challenge Facebook. It had huge internal importance inside Google and was pushed aggressively across the company’s ecosystem. But it failed to create the kind of organic social behaviour that made Facebook powerful. The consumer version was eventually shut down after low usage and privacy/security issues. Again, no project-level loss is disclosed, but the cost in engineering time, management attention and opportunity cost was likely very large.

Stadia was Google’s cloud gaming platform. It had an ambitious technological vision: high-quality gaming streamed from the cloud. But the service did not gain the user adoption Google expected and was shut down. The full cost is not disclosed, but a reasonable estimate would be hundreds of millions to low single-digit billions, including infrastructure, staff, content commitments and refunds. Some technology may have been repurposed, but as a consumer platform, Stadia failed.

Loon, the moonshot project designed to provide internet connectivity through high-altitude balloons, was also shut down. The vision was powerful, but the business was not commercially viable. Its losses were absorbed within Alphabet’s Other Bets segment and were likely in the hundreds of millions or more.

Titan Aerospace, Google’s drone-related connectivity project, was another discontinued moonshot. The project was shut down after technical and economic challenges. Again, the exact loss is undisclosed.

Google Fiber, or GFiber, sits somewhere between failure and useful experiment. It is a real service and still exists, but the original ambition of broad fibre rollout slowed significantly because the economics were difficult. Fibre infrastructure is expensive, slow and capital intensive. Google Fiber may have helped pressure incumbents and gave Google experience in connectivity, but it did not become a classic Google-scale financial success. It remains a mixed infrastructure bet.

Waymo is different from the failures, but it is still expensive and uncertain. It is one of Alphabet’s most promising long-term bets, but autonomous vehicles are extraordinarily capital intensive and slow to scale. Waymo’s cumulative spend is not separately disclosed, and its losses are included within Other Bets. The project could become very valuable, but it is not yet a mature profit engine. It is promising, but expensive.

Wiz and Intersect represent newer large bets. Wiz, announced at $32 billion, is intended to strengthen Google Cloud’s cybersecurity position. Intersect, announced at $4.8 billion, appears relevant to energy and data-centre infrastructure, which connects directly with the AI build-out. Both are too early to judge, but they show Alphabet moving into larger and more strategic acquisitions tied to Cloud and AI infrastructure.

The Biggest Visible Financial Mistake: Motorola

Motorola remains the cleanest example of a large, visible financial loss.

Google bought Motorola Mobility for $12.5 billion. It sold the handset business to Lenovo for $2.91 billion and the set-top box business to Arris for $2.35 billion. That leaves a simple cash gap of about $7.2 billion. Google retained patents, and some analysts estimated those patents were worth around $5.5 billion, so the net economic loss was not as simple as the headline numbers suggest. However, Motorola also produced operating losses while Google owned it. That is why the shareholder-impact estimate of $8 billion to $10 billion of drag is plausible.

The acquisition made strategic sense in one respect: it helped Google protect Android during the smartphone patent wars. But as an operating business, Motorola showed that Google was not naturally suited to running a traditional hardware manufacturer. It was a defensive move that carried a heavy financial cost.

The Most Expensive Ongoing Category: Other Bets

The individual moonshot numbers are mostly hidden, but Alphabet’s Other Bets segment gives us the best official view of the scale.

From 2017 to 2025, Other Bets produced cumulative operating losses of roughly $38.8 billion. This includes businesses such as Waymo, Verily, X-related projects, Access/GFiber and other experimental ventures. Other Bets revenue rose from $477 million in 2017 to $1.537 billion in 2025, but the losses remained substantial, including a $7.5 billion operating loss in 2025.

This does not mean that all $38.8 billion was wasted. Some of that money funded technologies that may still have option value. Waymo, for example, could still become significant. Verily may have strategic health potential. Some projects may have produced learning, patents, talent and infrastructure that benefited other parts of Alphabet.

But from a shareholder perspective, the message is clear. Alphabet has long used the enormous cash flow from Search and Ads to fund a large internal venture-capital portfolio.

The Magic Leap, Glass and Stadia Lesson

Magic Leap, Google Glass and Stadia are important because they reveal a recurring weakness.

Google is brilliant at infrastructure, search, data, advertising and machine intelligence. It is less consistent at creating emotionally compelling consumer hardware, entertainment experiences and social products.

Magic Leap was built on a powerful technological vision, but the consumer adoption system was not there. Google Glass had futuristic appeal, but people did not want to wear it in normal social life. Stadia had impressive cloud technology, but gamers did not adopt it at the required scale.

The pattern is clear: Google often understands what technology can do before it fully understands what people are willing to change in their lives.

That is a crucial lesson for AI as well. The technology may be remarkable, but the economics depend on adoption, pricing, trust, workflow change, regulation and habit formation. Technical possibility is not the same as commercial inevitability.

The Winners Paid for the Failures

The reason Alphabet could tolerate so many failed or mixed projects is that the winners were enormous.

YouTube alone now generates more than $60 billion annually across ads and subscriptions. Alphabet’s own 2025 numbers show YouTube advertising revenue of $40.4 billion, Google Cloud revenue of $58.7 billion, and total revenue of $385.9 billion.

That is why the capital allocation story is not simply “Google wasted money.”

A better summary is this: Google made a small number of extraordinary platform bets that created hundreds of billions in value, and used the resulting cash flow to fund a much larger number of experiments, many of which failed.

That is very different from a normal company. Most companies cannot afford to lose billions on moonshots. Google could, because Search and Ads were so powerful.

The Rough Totals

Across the major disclosed acquisitions discussed here, excluding the pending Wiz and Intersect deals, Alphabet appears to have spent roughly $40 billion to $45 billion. The pending Wiz and Intersect acquisitions add another $36.8 billion of announced deal value.

Other Bets produced around $38.8 billion of cumulative operating losses between 2017 and 2025. Motorola likely created a net drag of around $8 billion to $10 billion before adjusting for patent and tax value. Magic Leap likely created a paper loss for Google in the hundreds of millions, though the exact number is not public. Glass, Google+, Stadia, Loon, Titan, Ara and similar discontinued projects likely cost several billions combined, although much of that would have been embedded inside research and development or Other Bets rather than separately disclosed.

Against those losses, the value created by Android, YouTube, DoubleClick, AdMob, Maps and Waze is not separately reported, but is likely worth hundreds of billions in strategic value.

This is the paradox of Alphabet. It has wasted serious money and still created enormous value.

The Shareholder Lesson

Alphabet’s acquisition and project history is not reckless overall. It is better understood as a venture-capital model attached to one of the greatest cash machines in corporate history.

The company makes many bets. Some fail. Some are mediocre. A few become extraordinary. Those extraordinary winners have historically paid for the failures many times over.

But the shareholder concern is different now.

In the past, Alphabet could fund many experiments from internal cash flow. A failed Magic Leap investment, Google Glass, Google+, Stadia or Loon did not threaten the company. Even Motorola, while painful, was absorbable.

AI infrastructure is different.

AI is not a $500 million experiment or a $3 billion acquisition. It is a capital cycle involving data centres, chips, power, cooling, energy contracts, cloud capacity and constant model development. The scale can reach tens or hundreds of billions.

So the historical lesson for Alphabet shareholders is this: Google has earned the right to take big bets because some of its past bets were spectacular. But it has not earned the right to be blindly trusted on every capital-intensive project.

The company is brilliant when it strengthens its core platforms. It is weaker when it tries to manufacture new consumer behaviour, enter hardware-heavy markets, or build capital-intensive infrastructure without clear returns.

With AI, the key question is not: has Google wasted money before?

It has.

The better question is: is AI more like Android and YouTube — a platform shift Alphabet must own — or more like Motorola, Fiber, Loon and Stadia — a capital-heavy bet where the technology is real but the returns may disappoint?

That is the question shareholders should be asking now.

Shareholders Forgive Mistakes When the Direction Is Right

In many companies, the CEO, founder or top team can make mistakes and still retain shareholder support. They can buy the wrong company, launch the wrong product, hire the wrong leader, enter the wrong market, or spend money on experiments that do not work. Shareholders may complain, but they often remain forgiving if the overall direction of the company is still positive.

This is especially true when the core business is growing, cash flow is strong, the share price is rising, and the company still appears to be moving in the right direction. In that environment, failures are treated as the cost of ambition. They are seen as experiments. They are forgiven because the winners pay for the losers.

That has largely been the Alphabet story.

Google could afford Google Glass. It could afford Google+. It could afford Stadia. It could afford Loon, Titan, Magic Leap, and even the painful Motorola acquisition. These were expensive mistakes, but they did not break the company because the underlying engine was so powerful. Search and advertising continued to generate huge cash flows. YouTube grew. Android protected mobile distribution. Cloud expanded. The share price, over the long term, justified patience.

When the overall trend is positive, shareholders do not demand perfection. They demand direction.

But this is also where the danger begins.

Shareholders are forgiving of mistakes when those mistakes sit around the edge of a successful core. They are much less forgiving when the mistake appears to involve the core itself, or when the scale of the mistake becomes large enough to change the economics of the whole company.

That is why the AI infrastructure cycle matters.

A failed product like Google Glass is embarrassing, but survivable. A failed gaming platform like Stadia is costly, but survivable. A poor acquisition like Motorola is painful, but absorbable. But tens or hundreds of billions committed to AI infrastructure is not a side experiment. It is a strategic redirection of capital.

This is the real shareholder dilemma.

If Alphabet’s AI spending protects Search, grows Cloud, strengthens YouTube, deepens advertising, and creates new revenue streams, shareholders will forgive almost everything. They will say the company had to spend. They will say management was brave. They will say Alphabet understood the platform shift and acted early.

But if the spending produces lower margins, slower buybacks, dilution, rising depreciation, unclear monetisation and weaker free cash flow, shareholders may reinterpret the same behaviour very differently. What once looked like vision may start to look like overconfidence. What once looked like investment may start to look like capital indiscipline.

Shareholders do not punish every mistake. They punish the moment when mistakes reveal that the old story no longer works.

That is the question for Alphabet now.

Is AI spending simply the next chapter in Google’s long history of bold platform bets — like Android, YouTube and DeepMind?

Or is it the moment when Alphabet shifts from being a high-return, cash-generating platform company into a capital-hungry infrastructure company whose returns are harder to predict?

As long as the overall trend remains positive, shareholders will be patient. But if the trend changes, the market will not judge Alphabet by its ambition. It will judge it by the returns on the capital it has deployed.